Why You Should Rebalance your Investment Portfolio

Last Updated: May 05, 2015

At some point in time you might have heard a familiar phrase used among financial advisers when they talk about building a portfolio, “Don’t put all your eggs in one basket.” Many times they are referring to the importance of having an asset allocation strategy.

An asset allocation strategy should represent the risk an investor is willing to take by investing monies ‘eggs’ in the various asset classes ‘baskets’ for a desired potential return. How many ‘eggs’ you put in each ‘basket’ will be influenced by many factors including how comfortable you are with risk, what goals you are trying to achieve, and the time frame available to achieve those goals. Having multiple asset classes represented in a portfolio can help an investor balance out the risk/reward trade off as they plan to meet their goals.

Once the strategy is established and investment chosen, you will want to monitor and review over time. Some ‘baskets’ will fill up with ‘eggs’ faster than others; some might even lose some ‘eggs’ from time to time. The asset classes in your portfolio may not move in the same direction at the same time or by the same amounts. Over a period of time the amount of ‘eggs’ in each ‘basket’ may look drastically different then how it started; these shifts can impact how your portfolio behaves and the risk that you are taking, which could impact your retirement plan. Rebalancing can help keep your portfolio inline by moving the ‘eggs’ between the ‘baskets’ back to your original allocation.

Let’s look at an example of how rebalancing works.

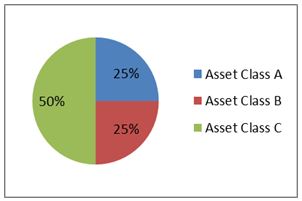

What if you originally set up an asset allocation strategy that had 25% invested in Asset Class A, 25% invested in Asset Class B and 50% invested in Asset Class C (figure 1).

Figure 1

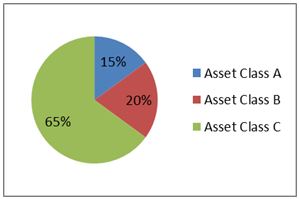

However because the asset classes didn’t earn the same amount over time, you notice that the allocation had shifted to 15% in Asset Class A, 20% in Asset Class B, and 65% in Asset Class C (figure 2).

Figure 2

The current portfolio looks completely different. What if asset class C has more risk of declining? You have more exposure to that risk now and might only be comfortable with 50% of our portfolio subject to that risk. You should rebalance the portfolio. To rebalance, you would sell part of the investment in asset class C and use it to purchase more of Asset Class A and B to bring your portfolio back to its original allocation.

You might consider rebalancing periodically on a quarterly, semi-annual, or annual basis. Keep in mind, the longer the time frame between each rebalance, the more potential there is for a shift further away from your original target allocation. A more involved method for deciding when to rebalance is to set a range that you are comfortable allowing your investments to fluctuate. For example you might want 10% in a particular asset class. You may choose only to rebalance back to the 10% target if the asset class shifts +/- 5% from the target.

Work with a CERTIFIED FINANCIAL PLANNER ™ professional on a rebalancing strategy to help maintain your desired risk level. They can help keep your asset allocation from shifting for longer periods of time or beyond an investment fluctuation range than what you are comfortable with.

When was the last time you reviewed your portfolio allocation? To discuss your asset allocation strategy with a CERTIFIED FINANCIAL PLANNER™ professional, contact Pension Consultants’ RetireAdvisers® Team at 1-800-234-9584.

PCI’s archived blog entries are dated, the rules and statutes referenced may have changed. The analysis or guidance within these blog entries may have become stale, dated, or no longer accurate. PCI will not update or change these entries to reflect the latest analysis or development.

WRITTEN BY

Pension Consultants, Inc.

FREE DOWNLOAD

Read The First Chapter

Learn what it takes to build a successful retirement plan so your employees can retire on time and with dignity. A must read for any fiduciary.

Pension Consultants, Inc. is excited to be featured on NAPA’s 2024 ‘Nation’s Top DC Advisor Teams’ ranking! For 30 years, PCI has been mission-driven to improve the financial security of American workers. We accomplish this by helping our clients get their employees on track for a successful retirement. Based on the asset sizes of those who submitted to be included on the list, we are very proud to be among the top 100 advisers in the nation and the largest DC adviser based in Missouri.

American workers are financially struggling. They are worrying about unforeseen expenses and feeling uncertain about their futures. However, Secure 2.0’s PLESA provision is a promising solution to help. Check out PCI’s top 5 reasons why PLESA is a great idea…

We believe emergency savings accounts within 401(k) plans are one of the most significant developments in recent years to help close the savings gap and improve the financial security of the American workforce.