Archives

Third Quarter 2015 Capital Markets Update

Last Updated: October 09, 2015

Equity and fixed income markets were especially volatile during the third quarter of 2015 with the surprise Chinese de-valuation of their currency, the yuan. This made exports from the U.S. and other countries more expensive, hurting sales during the third quarter. We expect this volatility to continue as companies report third quarter results and provide their outlook for the remainder of the year. Investors remain concerned about the Fed raising interest rates, slower global growth, and a weaker-than-expected jobs report for the U.S.

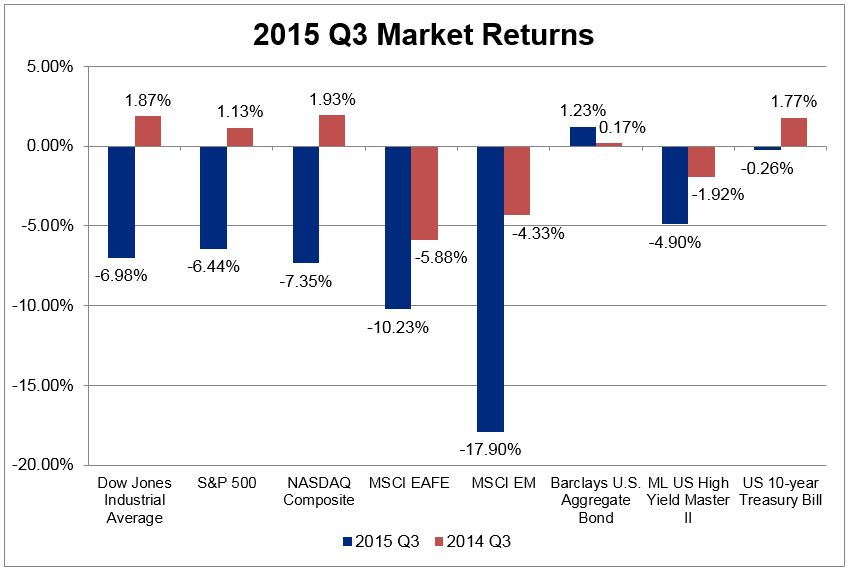

The major U.S. equity indexes posted negative returns for 2015’s third quarter1. The Dow Jones Industrial Average Index returned -6.98% compared to 1.87% a year ago. The broader S&P 500 Index returned of -6.44% compared to 1.13% a year ago. The Nasdaq Composite Index returned -7.35% compared to 1.93% a year ago.

Foreign markets were even more volatile as anticipation of higher interest rates is especially harmful to emerging markets. Concerns over the European Union, unrest in the Middle East, and bolder competition from China, Russia, and Latin America caused investors to take on less risk. China was held out as the last hope for international growth but those hopes were dashed as current conditions and the outlook for growth fell below expectations.

The non-U.S. equity market for companies in developed countries, as measured by the MSCI EAFE NR USD Index, returned -10.23% for the third quarter compared to -5.88% a year ago. Emerging market equities, as measured by the MSCI EM NR USD Index, which are more sensitive to an increase in interest rates, returned -17.90% compared to -4.33% a year ago.

Fixed income markets remained attractive for investors wanting less risk in “safe havens” like U.S. Treasury securities. The broad-based Barclays U.S. Aggregate Bond Index returned 1.23% for the third quarter compared to 0.17% a year ago. Riskier bonds, as measured by the ML US High Yield Master II Index, returned -4.90% compared to -1.92% a year ago. The more conservative US 10-year Treasury Bill index also posted a negative return of -0.26% for the third quarter compared to 1.77% a year ago.

Pension Consultants believes investors should review their portfolios at least once per year to determine if the mix of equities, fixed income and cash in the portfolio remains appropriate. Recent market activity may have caused portfolios to become out-of-balance compared to the investors’ risks appetite. This imbalance compared to the original portfolio intentions should cause investors to revisit their portfolios and rebalance as necessary.

Our Investment Services team can help identify investment funds that are in line with your retirement plan goals, while mitigating risk. To learn more, contact a Pension Consultants Investment Consultant at 800-234-9584 or email investmentservices@pension-consultants.com.

Fixed income markets remained attractive for investors wanting less risk in “safe havens” like U.S. Treasury securities. The broad-based Barclays U.S. Aggregate Bond Index returned 1.23% for the third quarter compared to 0.17% a year ago. Riskier bonds, as measured by the ML US High Yield Master II Index, returned -4.90% compared to -1.92% a year ago. The more conservative US 10-year Treasury Bill index also posted a negative return of -0.26% for the third quarter compared to 1.77% a year ago.

Pension Consultants believes investors should review their portfolios at least once per year to determine if the mix of equities, fixed income and cash in the portfolio remains appropriate. Recent market activity may have caused portfolios to become out-of-balance compared to the investors’ risks appetite. This imbalance compared to the original portfolio intentions should cause investors to revisit their portfolios and rebalance as necessary.

Our Investment Services team can help identify investment funds that are in line with your retirement plan goals, while mitigating risk. To learn more, contact a Pension Consultants Investment Consultant at 800-234-9584 or email investmentservices@pension-consultants.com.

Fixed income markets remained attractive for investors wanting less risk in “safe havens” like U.S. Treasury securities. The broad-based Barclays U.S. Aggregate Bond Index returned 1.23% for the third quarter compared to 0.17% a year ago. Riskier bonds, as measured by the ML US High Yield Master II Index, returned -4.90% compared to -1.92% a year ago. The more conservative US 10-year Treasury Bill index also posted a negative return of -0.26% for the third quarter compared to 1.77% a year ago.

Pension Consultants believes investors should review their portfolios at least once per year to determine if the mix of equities, fixed income and cash in the portfolio remains appropriate. Recent market activity may have caused portfolios to become out-of-balance compared to the investors’ risks appetite. This imbalance compared to the original portfolio intentions should cause investors to revisit their portfolios and rebalance as necessary.

Our Investment Services team can help identify investment funds that are in line with your retirement plan goals, while mitigating risk. To learn more, contact a Pension Consultants Investment Consultant at 800-234-9584 or email investmentservices@pension-consultants.com.