Archives

Sequence of Returns Risk

Last Updated: April 10, 2014

One of the greatest risks to a successful retirement is out-living your assets. This could be caused by unaccounted-for inflation, uninsured medical expenses, or just living a lifestyle your assets cannot support for the long term. But sometimes you can save tenaciously, plan fervently, live frugally, adhere to all commonly accepted investing principles and still have your retirement nest egg dwindle. One possible cause of this scenario could be the risk from your sequence of returns.

Sequence of returns risk can be summarized as the risk from the order in which investment returns occur and the impact it has on the longevity of withdrawals available during retirement. Table 1 shows a very basic example:

Retiree A and Retiree B both retired with $1,000,000 and are withdrawing $4,000 per month. Furthermore, they both experienced the exact same returns which averaged 7% per year, yet Retiree A’s account balance had $41,000 more than Retiree B’s after three years of retirement. How did that happen? The answer is sequence of returns. Retiree B, whose down year in the market happened early in retirement will end up with less than Retiree A, whose down year happened later in retirement. In Table 1, you can see the impact over just three years; the impact can be exponentially larger over an entire 30-year retirement.

One thing to note is that the sequence of returns will not have any impact on a buy-and-hold portfolio. If you do not add or withdraw money during the time period, then two portfolios with the same average return will end with an identical account balance, regardless of the order of investment returns during the period. Sequence of returns risk only appears when you are actively drawing down a portfolio.

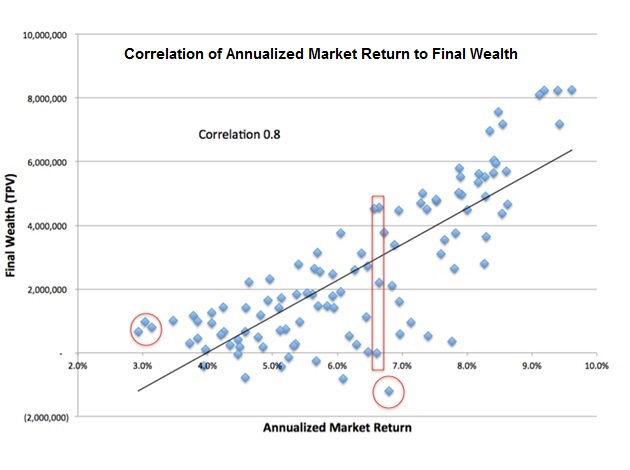

You may have heard the reasoning that only withdrawing 4% to 5% of your starting retirement value should guarantee success since the stock market has historically gone up by 8% to10%, and that as long as the market averages over 4.5%, you’ll be set. Well, let’s look at what would have happened to a typical retiree over the last 100+ years. Beginning in 1871, the S&P 500 has had a compound annual growth rate of 8.92%. According to research compiled by The Retirement Café, when we look at rolling 30-year returns of the S&P 500 to represent the average retirement, beginning in 1871, there are 108 such periods. However, depending on when you actually retired and the sequence of investment returns you experienced (especially early in your retirement), you could have surprisingly different results.

Retiree A and Retiree B both retired with $1,000,000 and are withdrawing $4,000 per month. Furthermore, they both experienced the exact same returns which averaged 7% per year, yet Retiree A’s account balance had $41,000 more than Retiree B’s after three years of retirement. How did that happen? The answer is sequence of returns. Retiree B, whose down year in the market happened early in retirement will end up with less than Retiree A, whose down year happened later in retirement. In Table 1, you can see the impact over just three years; the impact can be exponentially larger over an entire 30-year retirement.

One thing to note is that the sequence of returns will not have any impact on a buy-and-hold portfolio. If you do not add or withdraw money during the time period, then two portfolios with the same average return will end with an identical account balance, regardless of the order of investment returns during the period. Sequence of returns risk only appears when you are actively drawing down a portfolio.

You may have heard the reasoning that only withdrawing 4% to 5% of your starting retirement value should guarantee success since the stock market has historically gone up by 8% to10%, and that as long as the market averages over 4.5%, you’ll be set. Well, let’s look at what would have happened to a typical retiree over the last 100+ years. Beginning in 1871, the S&P 500 has had a compound annual growth rate of 8.92%. According to research compiled by The Retirement Café, when we look at rolling 30-year returns of the S&P 500 to represent the average retirement, beginning in 1871, there are 108 such periods. However, depending on when you actually retired and the sequence of investment returns you experienced (especially early in your retirement), you could have surprisingly different results.

Retiree A and Retiree B both retired with $1,000,000 and are withdrawing $4,000 per month. Furthermore, they both experienced the exact same returns which averaged 7% per year, yet Retiree A’s account balance had $41,000 more than Retiree B’s after three years of retirement. How did that happen? The answer is sequence of returns. Retiree B, whose down year in the market happened early in retirement will end up with less than Retiree A, whose down year happened later in retirement. In Table 1, you can see the impact over just three years; the impact can be exponentially larger over an entire 30-year retirement.

One thing to note is that the sequence of returns will not have any impact on a buy-and-hold portfolio. If you do not add or withdraw money during the time period, then two portfolios with the same average return will end with an identical account balance, regardless of the order of investment returns during the period. Sequence of returns risk only appears when you are actively drawing down a portfolio.

You may have heard the reasoning that only withdrawing 4% to 5% of your starting retirement value should guarantee success since the stock market has historically gone up by 8% to10%, and that as long as the market averages over 4.5%, you’ll be set. Well, let’s look at what would have happened to a typical retiree over the last 100+ years. Beginning in 1871, the S&P 500 has had a compound annual growth rate of 8.92%. According to research compiled by The Retirement Café, when we look at rolling 30-year returns of the S&P 500 to represent the average retirement, beginning in 1871, there are 108 such periods. However, depending on when you actually retired and the sequence of investment returns you experienced (especially early in your retirement), you could have surprisingly different results.