Archives

Using Match Structures to Improve Retirement Readiness

Last Updated: November 26, 2014

Most plan sponsors/employers would agree that the ultimate goal of a company-sponsored retirement plan is to help participants better prepare for life after their working career is over. With that in mind, many employers offer a company match to help encourage employees to save more for the future.

Unfortunately, there can be an unintended consequence of the employer match. Participants may abandon any attempt to use their retirement goals or projected income needs as the basis for how much they need to set aside for the future. Instead, they may use the company match as the deciding factor to determine how much to save and limit their contributions to the level of that match.

In my experience of providing enrollment education meetings, the one overwhelming question I hear from employees is simply, “What’s the match?” It’s not, “How much should I save to replace my income?”, or “How might I invest to reach my goals?” Instead, they only want to know the minimum amount they must contribute to receive the full benefit of the match.

The problem with basing contributions on the match is that it leaves many participants short of their retirement income needs. Many financial planners have a rule of thumb that individuals need to be saving anywhere from 10%-15% of their income for retirement, yet the average deferral rate is about 6%.

The good news is that employers can take notice of this behavior and use it to the participants’ advantage, creating the best solution possible to help them prepare for retirement. A well-designed match structure can be a powerful tool to encourage employees to save more for their future.

Granted, an employer must consider how much a match program will cost before deciding how big of a benefit to provide. But once the level of available resources is known, we recommend focusing on the behavioral outcome desired from the participant.

For example, let’s say a company decides 3% of employee’s income is an acceptable expense for their matching benefits program. How might that match be offered to have the greatest impact on participant behavior, keeping in mind that most employees save only the amount needed to receive the match?

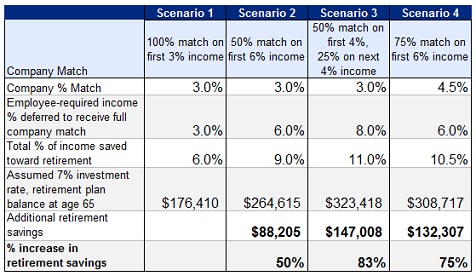

Now consider how a hypothetical employee, John Smith, might benefit from different match structures. John is 35 years old, earns $30,000 a year, and will continue to work until age 65. He plans to save just enough to receive the full company match.

Scenario 1: With a dollar-for-dollar company match, John will double his 3% salary deferral, saving 6% of his total income towards retirement. If we assume an investment return of 7%, John would have a balance of $176,410 at age 65.

Scenario 2: With a 50% match, John will need to defer more of his income to receive the additional 3% available from his employer. If he simply wants the same total benefit as before, John will need to save 4% of his income. John’s 4% plus the employer’s 2% provides 6% total savings for retirement. However, if John is able to save the full 6% and receive the 3% match for a total of 9% savings, he could benefit from an additional $88,205 at retirement. Although this is an improvement, in this scenario, John is still shy of saving within the 10%-15% of income most financial planners would suggest.

Scenario 3: Another option would be to create a tiered match structure. In this scenario, the employer is offering a 50% match on the first 4% of compensation, and a 25% match on next 4%. John’s employer would be providing him with the same 3% match but would require him to save 8% of his income. With a total of 11% of income being contributed John is in now in the 10%-15% range. By the time John turns 65, he’d have a retirement account balance of $323,418. That’s much better than the $176,410 he’d have from the first scenario where his total contribution totaled 6%.

Scenario 4: Since not all employees will choose to increase their deferrals to receive the new full match, a plan sponsor might be able to offer a higher match structure without seeing a dramatic increase in cost. Those who defer the full amount could receive an increased benefit as a result. For example, if John’s employer decides to offer a 75% match on the first 6% of income, his total contributions would increase to 10.5%, and his projected account balance at age 65 could grow to $308,717.

But what about Non-Elective Contributions?

Making non-elective employer contributions into a retirement plan is another great way to reward employees. These contributions are great to have in addition to providing a company match. Be careful though if this is the only type of contribution made, employees could get the wrong idea and think there isn’t a need for them to save as well.

The way a company match is structured can provide a dramatic difference in retirement readiness outcomes. By focusing on the behavioral outcomes desired from participants and building match structures accordingly, plan sponsors can help participants better prepare for their retirement years.

Plan sponsors should review their match structure to determine if there is a more effective way to help participants prepare for retirement. To review your current match structure and possible alternatives to best help your employees prepare for retirement, contact one of Pension Consultants’ CERTIFIED FINANCIAL PLANNER™ professionals at 800-234-9584 for assistance.

PCI’s archived blog entries are dated, the rules and statutes referenced may have changed. The analysis or guidance within these blog entries may have become stale, dated, or no longer accurate. PCI will not update or change these entries to reflect the latest analysis or development.

Scenario 1: With a dollar-for-dollar company match, John will double his 3% salary deferral, saving 6% of his total income towards retirement. If we assume an investment return of 7%, John would have a balance of $176,410 at age 65.

Scenario 2: With a 50% match, John will need to defer more of his income to receive the additional 3% available from his employer. If he simply wants the same total benefit as before, John will need to save 4% of his income. John’s 4% plus the employer’s 2% provides 6% total savings for retirement. However, if John is able to save the full 6% and receive the 3% match for a total of 9% savings, he could benefit from an additional $88,205 at retirement. Although this is an improvement, in this scenario, John is still shy of saving within the 10%-15% of income most financial planners would suggest.

Scenario 3: Another option would be to create a tiered match structure. In this scenario, the employer is offering a 50% match on the first 4% of compensation, and a 25% match on next 4%. John’s employer would be providing him with the same 3% match but would require him to save 8% of his income. With a total of 11% of income being contributed John is in now in the 10%-15% range. By the time John turns 65, he’d have a retirement account balance of $323,418. That’s much better than the $176,410 he’d have from the first scenario where his total contribution totaled 6%.

Scenario 4: Since not all employees will choose to increase their deferrals to receive the new full match, a plan sponsor might be able to offer a higher match structure without seeing a dramatic increase in cost. Those who defer the full amount could receive an increased benefit as a result. For example, if John’s employer decides to offer a 75% match on the first 6% of income, his total contributions would increase to 10.5%, and his projected account balance at age 65 could grow to $308,717.

But what about Non-Elective Contributions?

Making non-elective employer contributions into a retirement plan is another great way to reward employees. These contributions are great to have in addition to providing a company match. Be careful though if this is the only type of contribution made, employees could get the wrong idea and think there isn’t a need for them to save as well.

The way a company match is structured can provide a dramatic difference in retirement readiness outcomes. By focusing on the behavioral outcomes desired from participants and building match structures accordingly, plan sponsors can help participants better prepare for their retirement years.

Plan sponsors should review their match structure to determine if there is a more effective way to help participants prepare for retirement. To review your current match structure and possible alternatives to best help your employees prepare for retirement, contact one of Pension Consultants’ CERTIFIED FINANCIAL PLANNER™ professionals at 800-234-9584 for assistance.

PCI’s archived blog entries are dated, the rules and statutes referenced may have changed. The analysis or guidance within these blog entries may have become stale, dated, or no longer accurate. PCI will not update or change these entries to reflect the latest analysis or development.

Scenario 1: With a dollar-for-dollar company match, John will double his 3% salary deferral, saving 6% of his total income towards retirement. If we assume an investment return of 7%, John would have a balance of $176,410 at age 65.

Scenario 2: With a 50% match, John will need to defer more of his income to receive the additional 3% available from his employer. If he simply wants the same total benefit as before, John will need to save 4% of his income. John’s 4% plus the employer’s 2% provides 6% total savings for retirement. However, if John is able to save the full 6% and receive the 3% match for a total of 9% savings, he could benefit from an additional $88,205 at retirement. Although this is an improvement, in this scenario, John is still shy of saving within the 10%-15% of income most financial planners would suggest.

Scenario 3: Another option would be to create a tiered match structure. In this scenario, the employer is offering a 50% match on the first 4% of compensation, and a 25% match on next 4%. John’s employer would be providing him with the same 3% match but would require him to save 8% of his income. With a total of 11% of income being contributed John is in now in the 10%-15% range. By the time John turns 65, he’d have a retirement account balance of $323,418. That’s much better than the $176,410 he’d have from the first scenario where his total contribution totaled 6%.

Scenario 4: Since not all employees will choose to increase their deferrals to receive the new full match, a plan sponsor might be able to offer a higher match structure without seeing a dramatic increase in cost. Those who defer the full amount could receive an increased benefit as a result. For example, if John’s employer decides to offer a 75% match on the first 6% of income, his total contributions would increase to 10.5%, and his projected account balance at age 65 could grow to $308,717.

But what about Non-Elective Contributions?

Making non-elective employer contributions into a retirement plan is another great way to reward employees. These contributions are great to have in addition to providing a company match. Be careful though if this is the only type of contribution made, employees could get the wrong idea and think there isn’t a need for them to save as well.

The way a company match is structured can provide a dramatic difference in retirement readiness outcomes. By focusing on the behavioral outcomes desired from participants and building match structures accordingly, plan sponsors can help participants better prepare for their retirement years.

Plan sponsors should review their match structure to determine if there is a more effective way to help participants prepare for retirement. To review your current match structure and possible alternatives to best help your employees prepare for retirement, contact one of Pension Consultants’ CERTIFIED FINANCIAL PLANNER™ professionals at 800-234-9584 for assistance.

PCI’s archived blog entries are dated, the rules and statutes referenced may have changed. The analysis or guidance within these blog entries may have become stale, dated, or no longer accurate. PCI will not update or change these entries to reflect the latest analysis or development.