Archives

The Care and Feeding of Your Retirement Plan Account

Last Updated: October 01, 2015

The three R’s of retirement plan maintenance: Review, Rebalance, and Reallocate

Remember when you were growing up and you got your first pet? You were so excited and you promised to take good care of it – and hopefully you did. In the same way, your retirement plan account needs your attention to stay healthy. “Set it and forget it” just doesn’t work. Without proper attention, your account, like your pet, could suffer malnutrition and not be adequate for your future needs. It could get sick so it doesn’t perform like you want it to. Or it could get hurt if it’s subjected to too much risk. Unlike your first pet, though, your retirement account is vitally important for your future, and you need to do everything you can to make sure it will still be there for you when you need it. You need to take care of your retirement plan account now, so it can take care of you later! Here are three specific areas to focus on when you care for your account – the three R’s of retirement plan maintenance: Review, Rebalance, and Reallocate. REVIEW: Once a quarter, review your account statement to make sure everything is in order, and then once a year meet with a financial professional to take a more in-depth look at how your money’s doing. Review the same things you might look for when caring for your pet:- Proper Conditions: Make sure your account is set up correctly. Is the contact information on your statement accurate? Are your salary deferrals and employer matches being recorded properly? Are your investments allocated the way you intend? Is your beneficiary information up-to-date?

- Proper Nutrition: Make sure you’re contributing enough to your account. Are you getting the full match from your employer? How much more could you be contributing if you really wanted to? How much should you be contributing to reach your retirement goals?

- Proper Exercise: Make sure your money is working as hard for you as you’ve been working for it. Does the performance of the funds in your account compare well to benchmarks? Does your mix of investments include enough market exposure? Are loans and distributions from your account hurting its overall performance?

- Proper Safety: Make sure your money is not exposed to excessive risk. Do you have too much equity in your portfolio? Is your portfolio properly diversified among various asset classes? How much risk are you willing to take in pursuit of higher returns?

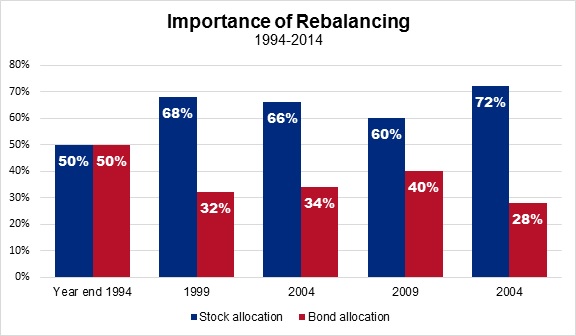

Source: © 2015 Morningstar. All Rights Reserved. Past performance is no guarantee of future results. Stocks: 50% large and 50% small stocks. Bonds: intermediate-term government bonds. This is for illustrative purposes only and not indicative of any investment. An investment cannot be made directly in an index.

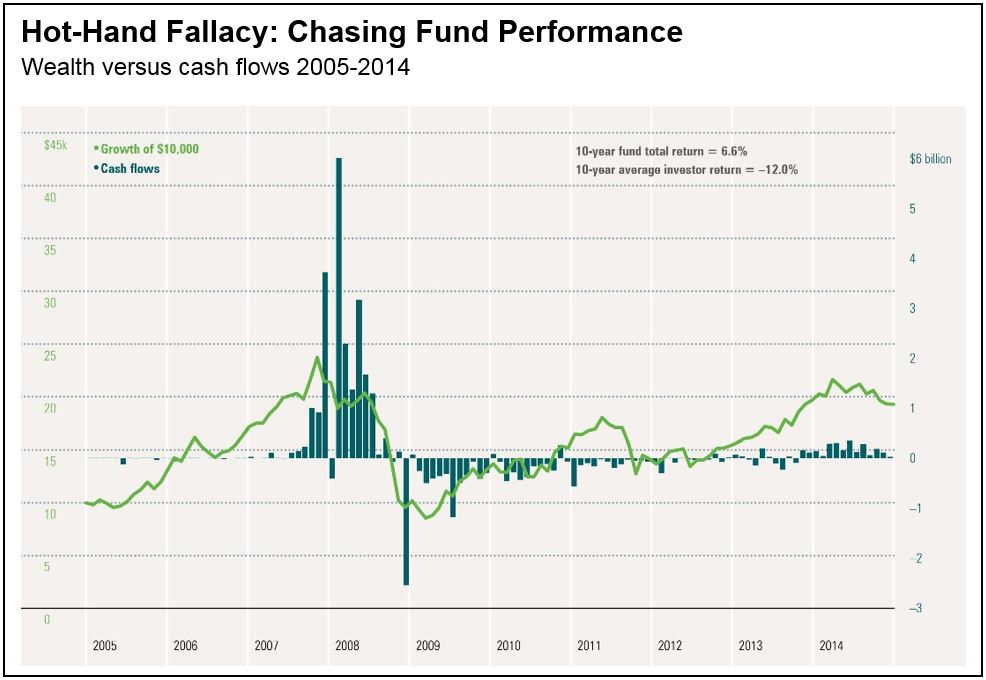

Thankfully, the solution is easy. Just harvest some of the growth from the over-performing areas and add it to the other funds until everything is back in balance. REALLOCATE: As you get closer to retirement, and sometimes for other reasons, your risk tolerance may change. For most people, it gets more conservative over time. Let’s say you used to feel comfortable with a 50/50 mix of stocks and bonds, but now you’d prefer only 25% of your money in stocks. Again, the solution is simple. Just move funds from the areas that you want reduced and add them to the areas where you’d like to see a greater allocation. One word of caution: Reallocating based on market conditions or on what you think the market is going to do is not recommended. That’s called timing the market, and it rarely works. For example, even though the stock market averaged 6.6% growth during the 10 years from 2005 through 2014, the average return of investors was negative 12%! That because people reacted emotionally to market conditions and tried to time the market.

One word of caution: Reallocating based on market conditions or on what you think the market is going to do is not recommended. That’s called timing the market, and it rarely works. For example, even though the stock market averaged 6.6% growth during the 10 years from 2005 through 2014, the average return of investors was negative 12%! That because people reacted emotionally to market conditions and tried to time the market.