We experienced a very quiet, low-volatility market for the first two months and 3 weeks of the 2nd quarter. Then the Brexit happened!

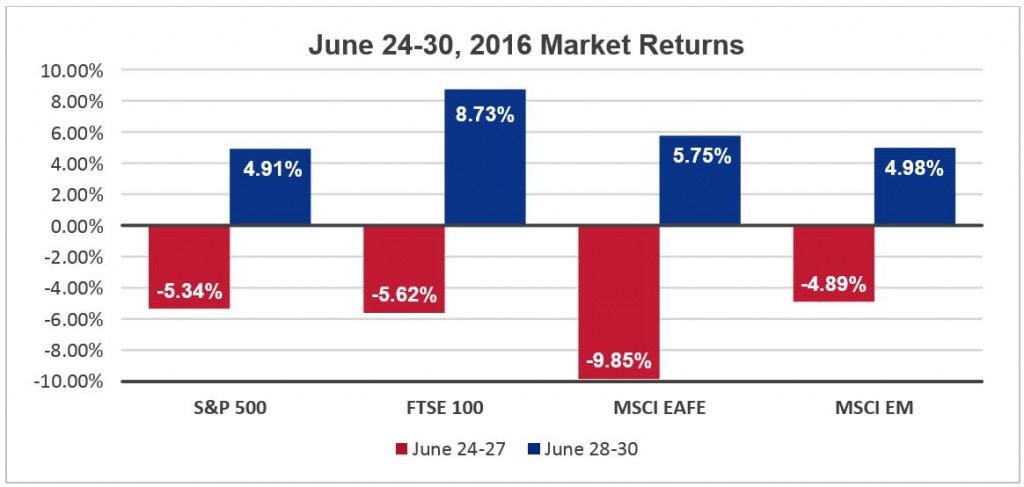

For most of the quarter, equity investors continued the trend of climbing the wall of worry. The quarter saw concerns over the job market (only 38,000 jobs created in May[1]), no growth in corporate earnings (for the 4th consecutive quarter), uncertainty over future Federal Reserve rate hikes, and anticipation of the British referendum over whether to stay in the European Union. But in the midst of all these concerns equity markets slowly climbed higher. It was not until June 24, when the surprise result came out of Britain to leave the EU, that the markets received a jolt of volatility.

Economic news in Q2 was mostly positive with strength in consumer and housing data offsetting the poor jobs number. First quarter gross domestic product (GDP) saw an upward revision from 0.5% to 1.1% during the quarter[2]. The Federal Reserve continued the trend of projecting higher interest rates just beyond the horizon. During Q1 2016, investors expected interest rates would increase between the April and June Fed meeting. As Q2 dawned, markets expected an interest rate increase in either July or September. Now as we enter Q3, the projection is for a rate increase in December at the earliest, and possibly not until 2017.

Source: Yahoo! Finance

The U.S. markets represented by the S&P 500 returned 2.46% for Q2, while foreign developed markets represented by the MSCI EAFE index returned -1.46% and emerging markets (MSCI EM index) gained 0.66%[3]. However, these muted returns belie the volatility witnessed in the last week of Q2.

On the fixed income side, the benchmark 10-year Treasury Bond saw its yield fall from 1.79% at the start of Q2 to 1.49% by the end[4]. The reduction in rates on intermediate and longer term bonds contributed to a 2.21% total return from the Barclays US Aggregate Bond index, while high yield bonds as represented by the BofAML High Yield Master II index returned 5.88%. Bonds saw much of their return come in the last week of Q2 as the Brexit vote resulted in a flight to safety highlighted by buying of U.S. Dollars, and U.S. Treasury Bonds.

The events of the 2nd quarter serve to remind investors that a dull market can still produce unexpected and dramatic swings up or down. It is important that portfolios are positioned appropriately for the risk tolerance and time horizon of the investor. If the recent volatility has caused you to question your current asset allocation, our Investment Services team can help. To learn more, contact a Pension Consultants Investment Consultant at 800-234-9584 or email investmentservices@pension-consultants.com.

I160711-1

[1] The Employment Situation–May 2016. Bureau of Labor Statistics, U.S. DOL, 6/3/16 [2]Gross Domestic Product: 1st Quarter 2016 (3rd Estimate), BEA, U.S. Dept. of Commerce, 6/28/16 [3] Index Returns as of 06/30/16, Morningstar.com [4]TNX Historical Prices|CBOE Interest Rate 10 Year T No Stock. Yahoo! Finance

PCI’s archived blog entries are dated, the rules and statutes referenced may have changed. The analysis or guidance within these blog entries may have become stale, dated, or no longer accurate. PCI will not update or change these entries to reflect the latest analysis or development.

WRITTEN BY

Pension Consultants, Inc.

FREE DOWNLOAD

Read The First Chapter

Learn what it takes to build a successful retirement plan so your employees can retire on time and with dignity. A must read for any fiduciary.

Pension Consultants, Inc. is excited to be featured on NAPA’s 2024 ‘Nation’s Top DC Advisor Teams’ ranking! For 30 years, PCI has been mission-driven to improve the financial security of American workers. We accomplish this by helping our clients get their employees on track for a successful retirement. Based on the asset sizes of those who submitted to be included on the list, we are very proud to be among the top 100 advisers in the nation and the largest DC adviser based in Missouri.

American workers are financially struggling. They are worrying about unforeseen expenses and feeling uncertain about their futures. However, Secure 2.0’s PLESA provision is a promising solution to help. Check out PCI’s top 5 reasons why PLESA is a great idea…

We believe emergency savings accounts within 401(k) plans are one of the most significant developments in recent years to help close the savings gap and improve the financial security of the American workforce.