Written By:

Cody Mendenhall, CFP®, Executive Director

Get Help:

Share this post:

Archives

A Closer Look at Target Date Funds

Last Updated: December 14, 2015

In 1978, Defined Contribution (DC) plans were first introduced. Unlike Defined Benefit (DB) plans, participants were given the freedom to choose a savings rate and their own asset allocation. However, participants also became wholly responsible for the risk of the investments and saving enough for retirement (i.e. making sure they don’t outlive their savings). Unfortunately, most plan participants were unequipped to make these decisions on their own. To mediate these concerns, target date funds became a Qualified Default Investment Option under the Pension Protection Act of 2006.

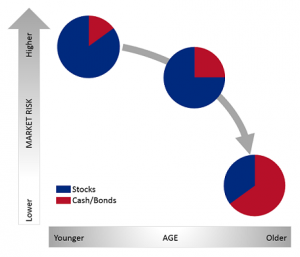

Target date funds automatically adjust asset allocation for plan participants. At the early stage participants have the lowest cash balance and the highest equity allocation. Having a high equity allocation exposes the participants to a high level of market risk (risk occurring from fluctuations within the market). However, high equity allocation helps alleviate longevity risk (the risk of outliving your assets) by exposing the participant to higher yielding investments at a younger age (allowing for the higher returns that will be compounded over a long time horizon).

Typically, at later stages (closer to retirement) participants have the highest cash balances and lowest equity allocation. On one hand, participants are exposed to lower market risk. On the other hand, they are exposed to increased longevity risk because of their decreased use of higher yielding investments.

It’s important to remember that retirement planning is not a “one size fits all” process. Programs that automatically adjust may not accommodate for every participant’s individual comfort level with market risk. Another thing to consider is that it is easy to skew asset allocations if the participant uses additional investment vehicles. Then consider what happens as participants near retirement. For some, it’s appropriate when their asset allocation automatically shifts to more cash/bonds. Yet others may still need both growth and income at that time, so they may need more of an equity component to stay on track. It becomes extremely difficult for one target date fund to meet the individual needs of each investor.

Work with a retirement plan consultant that can help empower your participants to make the right choice for them. You do this by first finding a consultant that looks for investment managers that can outperform an index on a consistent basis. Using this information, the consultant can then help facilitate proper asset allocation for your company’s retirement plan line-up. Finally, the consultant should be able to help your participants determine a suitable saving rate to meet their retirement goals.

To learn more about developing asset allocation strategies that can fit your participants’ needs, contact our Investment Services Team or RetireAdvisers® Team at 1-800-234-9584.

Target date funds automatically adjust asset allocation for plan participants. At the early stage participants have the lowest cash balance and the highest equity allocation. Having a high equity allocation exposes the participants to a high level of market risk (risk occurring from fluctuations within the market). However, high equity allocation helps alleviate longevity risk (the risk of outliving your assets) by exposing the participant to higher yielding investments at a younger age (allowing for the higher returns that will be compounded over a long time horizon).

Typically, at later stages (closer to retirement) participants have the highest cash balances and lowest equity allocation. On one hand, participants are exposed to lower market risk. On the other hand, they are exposed to increased longevity risk because of their decreased use of higher yielding investments.

It’s important to remember that retirement planning is not a “one size fits all” process. Programs that automatically adjust may not accommodate for every participant’s individual comfort level with market risk. Another thing to consider is that it is easy to skew asset allocations if the participant uses additional investment vehicles. Then consider what happens as participants near retirement. For some, it’s appropriate when their asset allocation automatically shifts to more cash/bonds. Yet others may still need both growth and income at that time, so they may need more of an equity component to stay on track. It becomes extremely difficult for one target date fund to meet the individual needs of each investor.

Work with a retirement plan consultant that can help empower your participants to make the right choice for them. You do this by first finding a consultant that looks for investment managers that can outperform an index on a consistent basis. Using this information, the consultant can then help facilitate proper asset allocation for your company’s retirement plan line-up. Finally, the consultant should be able to help your participants determine a suitable saving rate to meet their retirement goals.

To learn more about developing asset allocation strategies that can fit your participants’ needs, contact our Investment Services Team or RetireAdvisers® Team at 1-800-234-9584.

Target date funds automatically adjust asset allocation for plan participants. At the early stage participants have the lowest cash balance and the highest equity allocation. Having a high equity allocation exposes the participants to a high level of market risk (risk occurring from fluctuations within the market). However, high equity allocation helps alleviate longevity risk (the risk of outliving your assets) by exposing the participant to higher yielding investments at a younger age (allowing for the higher returns that will be compounded over a long time horizon).

Typically, at later stages (closer to retirement) participants have the highest cash balances and lowest equity allocation. On one hand, participants are exposed to lower market risk. On the other hand, they are exposed to increased longevity risk because of their decreased use of higher yielding investments.

It’s important to remember that retirement planning is not a “one size fits all” process. Programs that automatically adjust may not accommodate for every participant’s individual comfort level with market risk. Another thing to consider is that it is easy to skew asset allocations if the participant uses additional investment vehicles. Then consider what happens as participants near retirement. For some, it’s appropriate when their asset allocation automatically shifts to more cash/bonds. Yet others may still need both growth and income at that time, so they may need more of an equity component to stay on track. It becomes extremely difficult for one target date fund to meet the individual needs of each investor.

Work with a retirement plan consultant that can help empower your participants to make the right choice for them. You do this by first finding a consultant that looks for investment managers that can outperform an index on a consistent basis. Using this information, the consultant can then help facilitate proper asset allocation for your company’s retirement plan line-up. Finally, the consultant should be able to help your participants determine a suitable saving rate to meet their retirement goals.

To learn more about developing asset allocation strategies that can fit your participants’ needs, contact our Investment Services Team or RetireAdvisers® Team at 1-800-234-9584.

Target date funds automatically adjust asset allocation for plan participants. At the early stage participants have the lowest cash balance and the highest equity allocation. Having a high equity allocation exposes the participants to a high level of market risk (risk occurring from fluctuations within the market). However, high equity allocation helps alleviate longevity risk (the risk of outliving your assets) by exposing the participant to higher yielding investments at a younger age (allowing for the higher returns that will be compounded over a long time horizon).

Typically, at later stages (closer to retirement) participants have the highest cash balances and lowest equity allocation. On one hand, participants are exposed to lower market risk. On the other hand, they are exposed to increased longevity risk because of their decreased use of higher yielding investments.

It’s important to remember that retirement planning is not a “one size fits all” process. Programs that automatically adjust may not accommodate for every participant’s individual comfort level with market risk. Another thing to consider is that it is easy to skew asset allocations if the participant uses additional investment vehicles. Then consider what happens as participants near retirement. For some, it’s appropriate when their asset allocation automatically shifts to more cash/bonds. Yet others may still need both growth and income at that time, so they may need more of an equity component to stay on track. It becomes extremely difficult for one target date fund to meet the individual needs of each investor.

Work with a retirement plan consultant that can help empower your participants to make the right choice for them. You do this by first finding a consultant that looks for investment managers that can outperform an index on a consistent basis. Using this information, the consultant can then help facilitate proper asset allocation for your company’s retirement plan line-up. Finally, the consultant should be able to help your participants determine a suitable saving rate to meet their retirement goals.

To learn more about developing asset allocation strategies that can fit your participants’ needs, contact our Investment Services Team or RetireAdvisers® Team at 1-800-234-9584.