Archives

Second Quarter 2015 Capital Markets Update

Last Updated: July 16, 2015

Both domestic and foreign markets struggled during the second quarter of 2015 compared to last year due to:

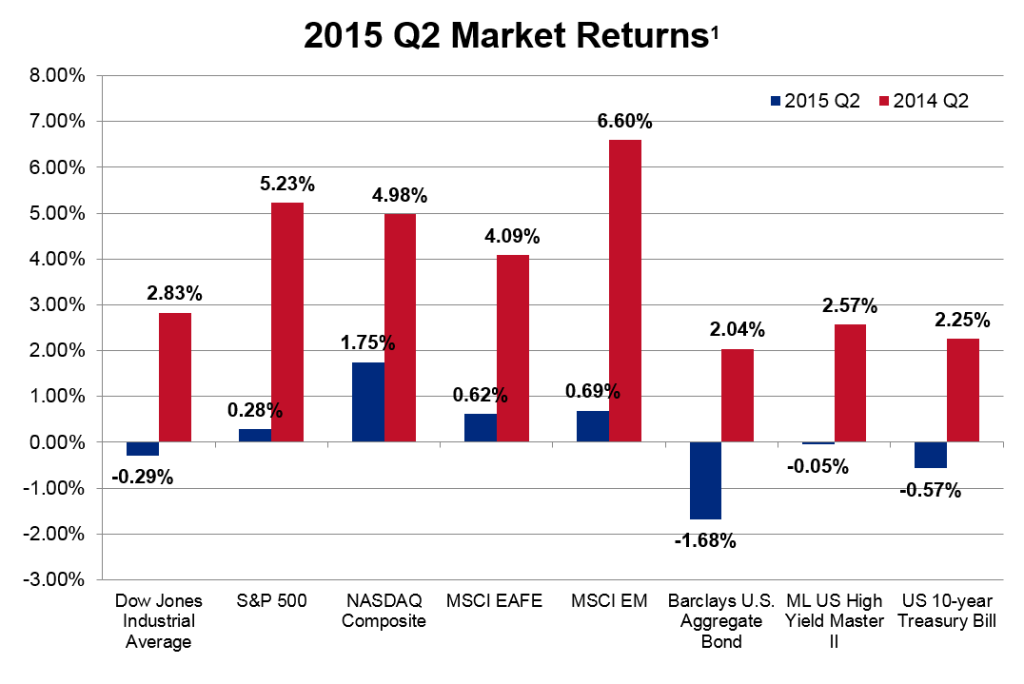

For the second quarter of 2015, the Dow Jones Industrial Average Index posted a -0.29% return compared to 2.83% a year ago. The broader S&P 500 Index posted a positive return of 0.28% compared to 5.23% a year ago. The Nasdaq Composite Index posted a positive 1.75% compared to 4.98% a year ago. While returns for the Nasdaq Composite Index benefitted from initial public offerings and merger & acquisition activity, the broader trend illustrates slower growth compared to last year.

The non-U.S. equity market for companies in developed countries, as measured by the MSCI EAFE NR USD Index, was only slightly positive returning 0.62% for the second quarter compared to 4.09% a year ago. Equities of companies in emerging market countries fared only slightly better, with the MSCI EM NR USD Index returning 0.69% return compared to 6.60% a year ago.

Fixed income markets remained volatile during the second quarter as the fear of higher interest rates was offset by investors looking for “safe havens” in U.S. Treasury securities. The broad-based Barclays U.S. Aggregate Bond Index returned -1.68% for the second quarter compared to 2.04% a year ago. Riskier bonds, as measured by the ML US High Yield Master II Index, returned -0.05% compared to 2.57% a year ago. The more conservative US 10-year Treasury Bill index also posted a negative return, of -0.57% for the second quarter compared to 2.25% a year ago. The negative returns across different sectors of the bond market illustrate broad based concerns that interest rates will be heading higher.

Pension Consultants believes that investors should review their portfolios to determine if the mix of equities, fixed income and cash in the portfolio remains appropriate. The current bull run in equities is over 6 years old, one of the longest in history, and may have resulted in some portfolios having more exposure to equities than is appropriate.

Our Investment Services team can help identify investments that are in line with your retirement plan goals, while mitigating the risk. To learn more, please contact an Investment Consultant at Pension Consultants. Call us at 800.234.9584 or email Investment Services Team.

For the second quarter of 2015, the Dow Jones Industrial Average Index posted a -0.29% return compared to 2.83% a year ago. The broader S&P 500 Index posted a positive return of 0.28% compared to 5.23% a year ago. The Nasdaq Composite Index posted a positive 1.75% compared to 4.98% a year ago. While returns for the Nasdaq Composite Index benefitted from initial public offerings and merger & acquisition activity, the broader trend illustrates slower growth compared to last year.

The non-U.S. equity market for companies in developed countries, as measured by the MSCI EAFE NR USD Index, was only slightly positive returning 0.62% for the second quarter compared to 4.09% a year ago. Equities of companies in emerging market countries fared only slightly better, with the MSCI EM NR USD Index returning 0.69% return compared to 6.60% a year ago.

Fixed income markets remained volatile during the second quarter as the fear of higher interest rates was offset by investors looking for “safe havens” in U.S. Treasury securities. The broad-based Barclays U.S. Aggregate Bond Index returned -1.68% for the second quarter compared to 2.04% a year ago. Riskier bonds, as measured by the ML US High Yield Master II Index, returned -0.05% compared to 2.57% a year ago. The more conservative US 10-year Treasury Bill index also posted a negative return, of -0.57% for the second quarter compared to 2.25% a year ago. The negative returns across different sectors of the bond market illustrate broad based concerns that interest rates will be heading higher.

Pension Consultants believes that investors should review their portfolios to determine if the mix of equities, fixed income and cash in the portfolio remains appropriate. The current bull run in equities is over 6 years old, one of the longest in history, and may have resulted in some portfolios having more exposure to equities than is appropriate.

Our Investment Services team can help identify investments that are in line with your retirement plan goals, while mitigating the risk. To learn more, please contact an Investment Consultant at Pension Consultants. Call us at 800.234.9584 or email Investment Services Team.

- uncertainty regarding the timing and size of an interest rate increase by the Fed,

- the potential impact on the European Union and the euro should Greece exit and drop the euro as currency, and

- lowered growth expectations for China which had been viewed as virtually immune from the problems affecting other regions of the world.

For the second quarter of 2015, the Dow Jones Industrial Average Index posted a -0.29% return compared to 2.83% a year ago. The broader S&P 500 Index posted a positive return of 0.28% compared to 5.23% a year ago. The Nasdaq Composite Index posted a positive 1.75% compared to 4.98% a year ago. While returns for the Nasdaq Composite Index benefitted from initial public offerings and merger & acquisition activity, the broader trend illustrates slower growth compared to last year.

The non-U.S. equity market for companies in developed countries, as measured by the MSCI EAFE NR USD Index, was only slightly positive returning 0.62% for the second quarter compared to 4.09% a year ago. Equities of companies in emerging market countries fared only slightly better, with the MSCI EM NR USD Index returning 0.69% return compared to 6.60% a year ago.

Fixed income markets remained volatile during the second quarter as the fear of higher interest rates was offset by investors looking for “safe havens” in U.S. Treasury securities. The broad-based Barclays U.S. Aggregate Bond Index returned -1.68% for the second quarter compared to 2.04% a year ago. Riskier bonds, as measured by the ML US High Yield Master II Index, returned -0.05% compared to 2.57% a year ago. The more conservative US 10-year Treasury Bill index also posted a negative return, of -0.57% for the second quarter compared to 2.25% a year ago. The negative returns across different sectors of the bond market illustrate broad based concerns that interest rates will be heading higher.

Pension Consultants believes that investors should review their portfolios to determine if the mix of equities, fixed income and cash in the portfolio remains appropriate. The current bull run in equities is over 6 years old, one of the longest in history, and may have resulted in some portfolios having more exposure to equities than is appropriate.

Our Investment Services team can help identify investments that are in line with your retirement plan goals, while mitigating the risk. To learn more, please contact an Investment Consultant at Pension Consultants. Call us at 800.234.9584 or email Investment Services Team.

For the second quarter of 2015, the Dow Jones Industrial Average Index posted a -0.29% return compared to 2.83% a year ago. The broader S&P 500 Index posted a positive return of 0.28% compared to 5.23% a year ago. The Nasdaq Composite Index posted a positive 1.75% compared to 4.98% a year ago. While returns for the Nasdaq Composite Index benefitted from initial public offerings and merger & acquisition activity, the broader trend illustrates slower growth compared to last year.

The non-U.S. equity market for companies in developed countries, as measured by the MSCI EAFE NR USD Index, was only slightly positive returning 0.62% for the second quarter compared to 4.09% a year ago. Equities of companies in emerging market countries fared only slightly better, with the MSCI EM NR USD Index returning 0.69% return compared to 6.60% a year ago.

Fixed income markets remained volatile during the second quarter as the fear of higher interest rates was offset by investors looking for “safe havens” in U.S. Treasury securities. The broad-based Barclays U.S. Aggregate Bond Index returned -1.68% for the second quarter compared to 2.04% a year ago. Riskier bonds, as measured by the ML US High Yield Master II Index, returned -0.05% compared to 2.57% a year ago. The more conservative US 10-year Treasury Bill index also posted a negative return, of -0.57% for the second quarter compared to 2.25% a year ago. The negative returns across different sectors of the bond market illustrate broad based concerns that interest rates will be heading higher.

Pension Consultants believes that investors should review their portfolios to determine if the mix of equities, fixed income and cash in the portfolio remains appropriate. The current bull run in equities is over 6 years old, one of the longest in history, and may have resulted in some portfolios having more exposure to equities than is appropriate.

Our Investment Services team can help identify investments that are in line with your retirement plan goals, while mitigating the risk. To learn more, please contact an Investment Consultant at Pension Consultants. Call us at 800.234.9584 or email Investment Services Team.