Archives

The Tools Your Retirement Plan May Be Missing: Auto-Enrollment & Auto-Escalation

Last Updated: June 22, 2017

What are your goals for your retirement plan? Are you a plan sponsor reviewing your plan and wondering to yourself, “Why is my plan not performing competitively against others,” or even more so, “How do I increase employee participation in my retirement plan?”

The answer could be, as we will outline in this post, something as simple as adding auto features to your plan design.

Each plan sponsor should consider their goals for their retirement plan, and then review its plan design to ensure that it is helping to meet those goals. One primary goal for retirement plans is to assist employees in overall retirement readiness. Your vision of retirement readiness for participants starts with ensuring that employees are saving for retirement. A retirement plan cannot benefit the employee that is not participating. A retirement plan cannot perform to the best of its ability without participants to drive success. This retirement readiness goal is highly impacted not only by employees not participating, but also by how much the employee is saving for retirement. If the employee is in the plan, but not deferring more than a minimal amount, then they cannot expect to be retirement ready.

Plan sponsors who create retirement plans with the goal of getting their employees’ retirement ready have begun adopting two plan features: automatic enrollment and auto-escalation. These two features have been shown to improve retirement readiness among participants, as well as meeting plan performance goals set by plan fiduciaries (retirement committees). According to the National Association of Retirement Plan Participants (“NARPP”), 56% of American companies now offer some kind of auto-enrollment program as of 2013, up 19% from 2005. [1] The trend continues to increase as the benefits of auto-enrollment become more clear, as shown in 2015 Vanguard study reported by BenefitsPro. [2] The study showed that auto enrollment doubled participation rates of examined respondents.

56% of American companies now offer some kind of auto-enrollment program as of 2013

Once participants are in the plan, it is imperative to save enough to get them retirement ready. This is where auto-escalation comes into effect. In many cases, plan sponsors add automatic enrollment starting at 3% of wages, which is a good start, but not even close to what many industry studies have indicated participants should, realistically, be saving. Those studies recommend anywhere from 10%-15% of their income to be sufficiently ready. To help participants get to this savings rate, many plan sponsors add an automatic escalation feature to increase the participants’ deferral percentage by 1% a year. A 2014 survey conducted by the Defined Contribution Institutional Investment Association found only 48 percent of employers offered plans with an auto-escalation feature.[3] With automatic escalation plans, participating employers are able to take an active role in the readiness of their participants.

One difficulty with plan design is anticipating the potential administrative burden. Often record keepers are capable of providing online demonstrations of what the plan sponsor’s duties would be with the addition of automatic enrollment and/or automatic escalation. Since record keepers tend to be paid based on the plan’s assets, they are motivated to assist in administering these plan design features as well.

The second concern when adding these plan provisions is what impact it will have on the match contribution cost. This is something you can ask your adviser to assist with. Advisers have the ability to run scenarios where the provisions would only apply to new participants, which has less of a cost impact. They can also look at the increase of match cost if the provisions applied to all plan participants.

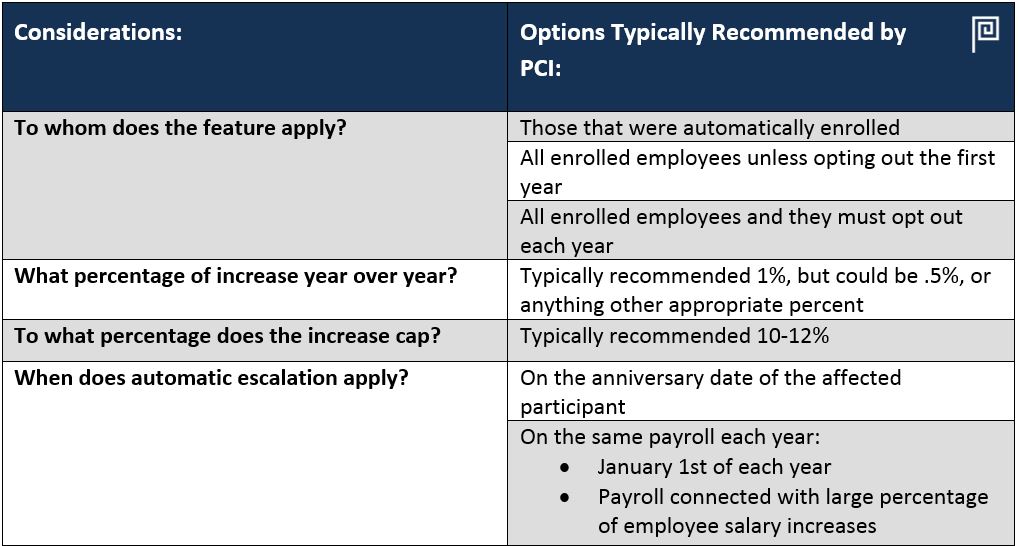

The bottom line is, if the goal is to a have a top performing retirement plan with participants successfully able to retire, adding automatic enrollment and automatic escalation should be considered. Below is a chart that can guide you through the decision-making process:

[1] “Automatic Enrollment: What Does It Mean,” National Association of Retirement Plan Participants, http://www.narpp.org/fiacademy/automatic-enrollment-what-does-mean#divID1, (June 15, 2017).

[2] Thorton, Nick, “Auto Enroll Doubles Participation Rates,” BenefitsPro, http://www.benefitspro.com/2015/01/20/auto-enroll-doubles-participation-rates?slreturn=1497890720, (June 15, 2017).

[3] Lucas, Lori, et al, “DCIIA Plan Sponsor Survey 2014: Focus on Automatic Plan Features,” DCIIA, https://www.transamericacenter.org/docs/default-source/resources/tcrs2015_wp_dciia_plan_sponsor_survey.pdf, pg. 3-6, (June 15, 2017).

[Photo Credit: Flickr | taxcredits-401k]

170616-1

PCI’s archived blog entries are dated, the rules and statutes referenced may have changed. The analysis or guidance within these blog entries may have become stale, dated, or no longer accurate. PCI will not update or change these entries to reflect the latest analysis or development.