Archives

2nd Quarter 2017 Capital Market Review

Last Updated: July 13, 2017

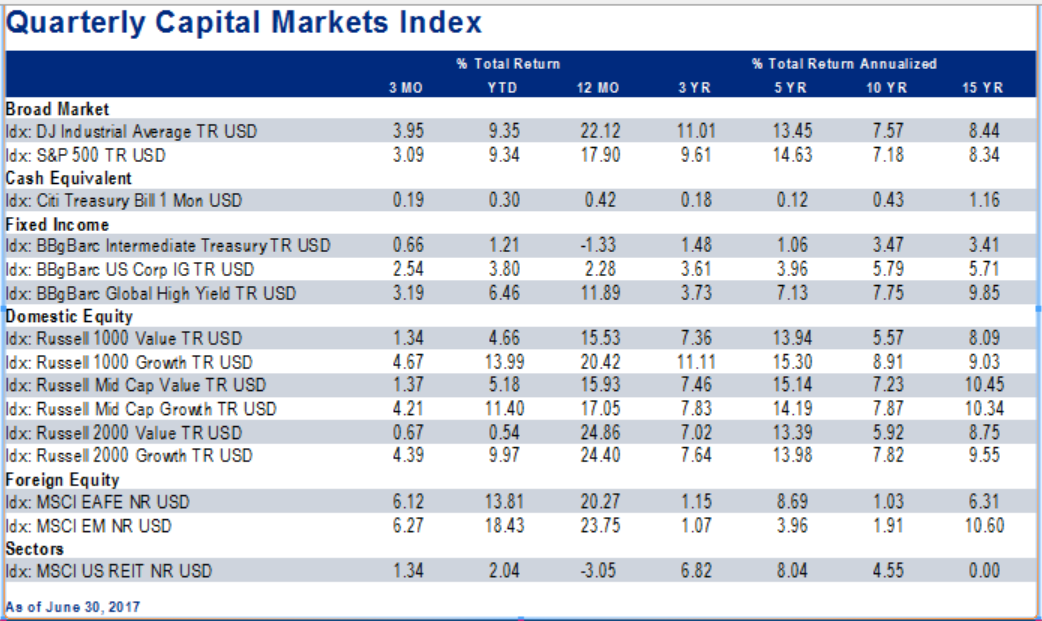

The 2nd quarter of 2017 continued the streak of new highs in equity markets. While this bull market has already lasted longer than most; investors still seem to be overly cautious, expecting a pullback at any moment. However, this nervousness is likely the reason the pullback has not happened. The longer the nervousness continues, the longer the market can run. Aiding the uptrend continues to be improving corporate earnings, low unemployment, low interest rates, low inflation, and a much improved consumer balance sheet.

The Federal Reserve continued on their one-rate-hike-per-quarter path, and also began discussing reducing the size of their balance sheet. That process may begin later this year, but will likely be slow and take many years to normalize. The yield curve is getting flatter as the short end reacts to Fed rate hikes, while the long end focuses on low inflation rates. Energy continued to be the biggest laggard as oil prices returned to the low end of its range at levels not seen since early 2016.

For the first time in several quarters, the market paid less attention to politics, and instead celebrated improving corporate earnings. Growth investments continued beating value investments, and foreign investments continued the year-to-date trend of outperforming domestic markets. Equity market growth could continue as corporate earnings continue to improve following the best quarter for earnings growth in several years.

Fixed income also experienced robust returns in the quarter as interest rates did not climb as much as expected and credit spreads continued to tighten on the improving corporate picture. However, bond returns may be muted in the second half of the year as spreads are at the low end of historical ranges and rates are likely to move higher. If recent market volatility had caused you to question your current asset allocations, our Investment Services Team can help. To learn more, contact Pension Consultants Investment Consultants at 800-234-9584 or email investmentservices@pension-consultants.com.

Source: Index Returns as of 6/30/2017, Morningstar.com

Disclosure: Past performance is not indicative of future results.

170711-1

PCI’s archived blog entries are dated, the rules and statutes referenced may have changed. The analysis or guidance within these blog entries may have become stale, dated, or no longer accurate. PCI will not update or change these entries to reflect the latest analysis or development.